Turn on suggestions

Auto-suggest helps you quickly narrow down your search results by suggesting possible matches as you type.

Showing results for

Let's fix the incorrect amount on the sales account, Praset.

Handling your own financial reporting is vital to know how each one works.

With the cash basis of accounting, you record income as it's received and expenses as they're paid. Whereas the accrual basis of accounting, income, and expenses are recorded when they're billed and earned, regardless of when the money is actually received.

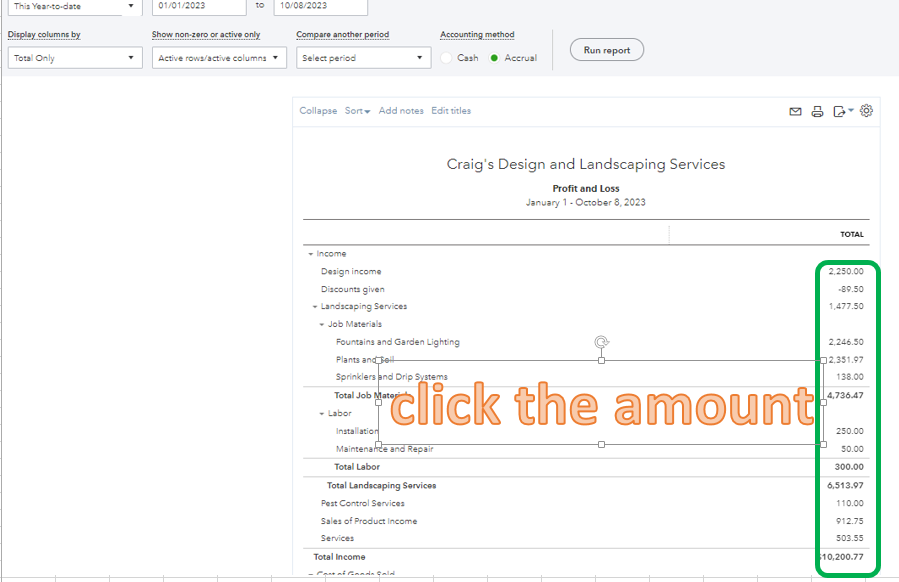

Normally, the Profit and Loss report shows all the sales transactions you entered on the income account. This means any transactions entered in QuickBooks will automatically generate when running reports. You'll want to drill down each transaction by clicking the amount so you'll be able to trace why it is showing an error amount. I've added a screenshot to guide you:

You can also go through this article to know what is reported on the Profit and Loss report: Why Are My Income And Expense Transactions Missing From My Profit And Loss Report?

In addition, check out some of our list of reports available for your QuickBooks Online (QBO) version. You can use some of them when comparing your transactions: Check out this article for more information: Reports Included In Your QuickBooks Online Subscription.

Feel free to comment below if you have any questions about your transactions or Profit and Loss report. I'll be one post away if you need further assistance.