Turn on suggestions

Auto-suggest helps you quickly narrow down your search results by suggesting possible matches as you type.

Showing results for

what can I need to check

Hello there, Anne. I understand how important it is to ensure your journal entries are reflected accurately, especially when it comes to your P&L report. Let’s check the accounts involved in the transaction and the report’s date range to ensure reversal amounts are accurately updated.

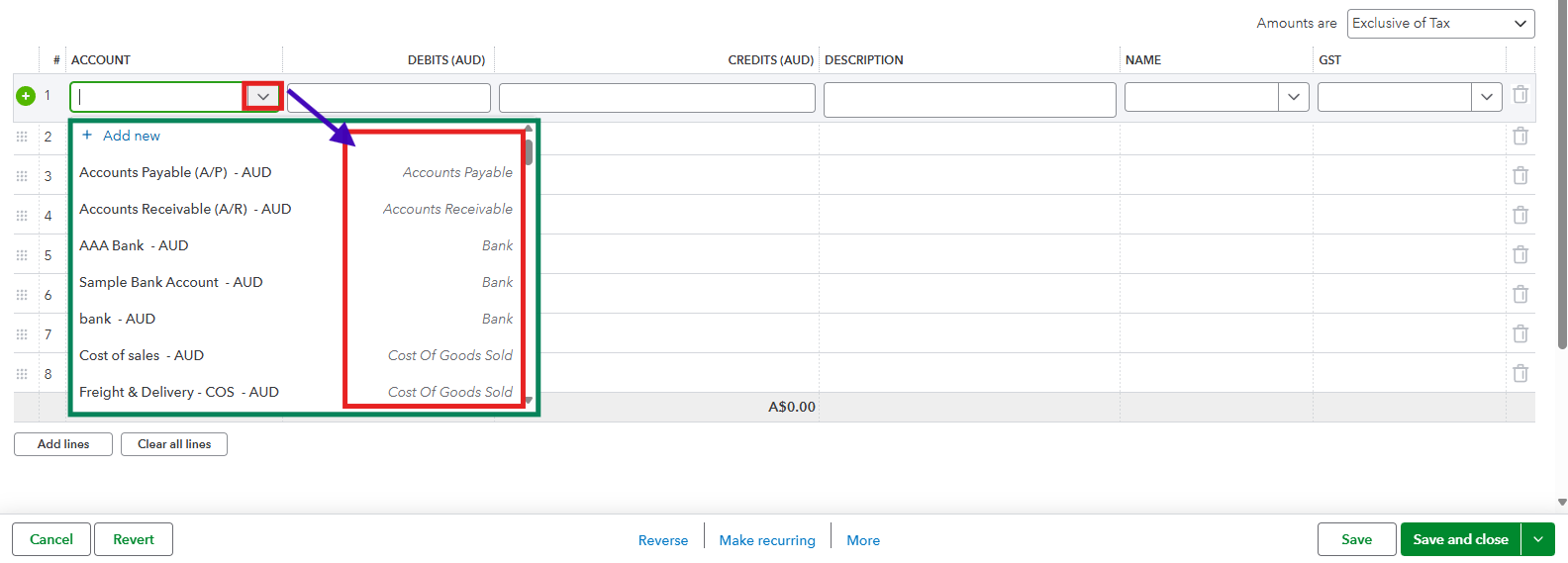

Accounts that appear in the Profit and Loss are classified as Income, Other Income, Cost of Sales, Expenses, and Other Expenses. An incorrect account selection in journal entries can be the reason reversal amounts aren't updating.

Here's how to review the entry:

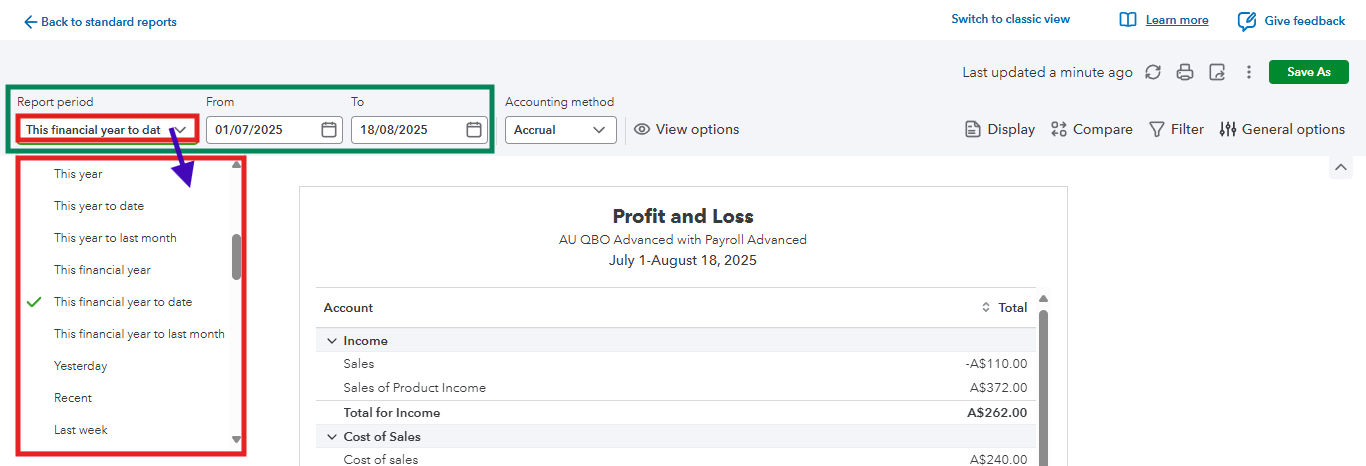

Once everything looks good, it's worth noting that setting the appropriate Report Period when generating the Profit and Loss is essential. Its date range should cover the dates of the journal entries. Here's a screenshot for your visual reference:

Please revisit this thread and tag us with your replies if you have other questions about journal entries and reports in QuickBooks Online. Rest assured, we’re always here to provide further assistance with any inquiries you may have.

You have clicked a link to a site outside of the QuickBooks or ProFile Communities. By clicking "Continue", you will leave the community and be taken to that site instead.

For more information visit our Security Center or to report suspicious websites you can contact us here